11 November 2017

Lithium battery manufacturers are beating each other up to grab their share of available Lithium

The demand for Lithium is pushing ASX listed share prices up. (updated 8 August 2019) Kidman resources share price now sitting at $1.90. Up from 50 cents two years ago.

The renewable revolution is driving the global vehicle industry toward electric. In the absence of alternative battery technologies, Lithium technology is currently the battery of choice. Problem is, the sudden increase in demand and the forecast growth in future demand is exceeding supply.

A huge investment in lithium production is underway, as well as research and development into alternative battery technologies. In the medium term, the price of lithium carbonate is escalating. The questions are how high will the price go? how long until supply catches up? and will a new technology emerge to replace lithium?

There are widely differing opinions about how the lithium market will pan out over the next 5 years and just how high prices will go. This article explores the situation.

Lithium is a prime ingredient in battery making, and so far, hasn’t been bettered for its two key properties; lightness and energy density.

These two properties make Lithium essential for manufacturing lightweight and compact batteries (compared to other battery technologies) suitable for electric vehicles, and portable electronic devices (laptops, cameras, phones, drones etc.)

But, now that major car makers (taking the lead from Tesla) and mega countries (notably India and China) are switching on to electric cars, demand for Lithium is skyrocketing and so is the price.

Current Lithium supplies globally are not sufficient to meet demand

In addition, Lithium is being used for solar battery installations, enabling solar panels to provide power 24 hours instead of just during daylight.

Lithium battery-making factories are being expanded and built everywhere, to supply batteries to fuel the gigantic demand. But they need more Lithium.

From a price in-elasticity perspective, here’s the magic bit. Lithium currently comprises less than 5% of the cost of manufacturing batteries.

That's less than 1% of the sticker price for an electric car. Consequently, battery makers can easily justify paying much higher prices to secure their share of the scarce resource. Prices are going through the roof.

What is Lithium?

Lithium is a metal and is the lightest metal on the periodic table and the lightest solid element.

Ranking number 3 on the periodic table, those with some basic knowledge of high school chemistry would appreciate the reason why it is so light. Lithium has only 3 protons and 4 neutrons making up its nucleus surrounded by 3 orbiting electrons. By comparison, Iron has 26 protons, 30 neutrons and 26 electrons.

Lithium has a very low density (0.534 g/cm3), comparable with pine wood.

Lithium is half the density of water. So it would float on water (if it were not too busy reacting with it).

It is a soft, silvery-white alkali metal. Like all alkali metals, lithium is highly reactive and flammable, and pure lithium must be stored in mineral oil. Lithium metal is soft enough to be cut with a knife. When cut open, it exhibits a metallic lustre, but moist air corrodes it quickly to a dull silvery grey, then black tarnish.

It never occurs freely in nature, but only in (usually ionic) compounds, such as pegmatitic minerals which were once the main source of lithium. Due to its solubility, it is present in ocean water and is commonly obtained from brines.

Lithium is the 33rd most abundant element in the earth's crust (copper, by comparison, ranks 26th); which would make you think it’s not too hard to find.

Well, it is easy to find, but difficult to cost-effectively extract into a usable form suitable for battery making.

So where does it come from? Two types of mining yield Lithium…

Hard rock lithium

Lithium can be mined using traditional hard rock mining. Hard rock mining is standard for mining minerals. Initially, suitable mine sites are searched, acquired and explored, followed by drilling and analysing core samples to confirm surface ore body survey techniques (magnetic anomaly, seismic studies etc.).

If results are promising, the search method switches to drilling and if pay dirt is hit, economic feasibility work is undertaken to prove up the resource. From there, all going well, the mine moves into production and processing lithium can begin. This process can take years - typically 10 to 20 years before first lithium ores are extracted.

After ore extraction, above-ground processing starts with ore crushing, followed by froth flotation concentration, hydro-metallurgy and precipitation from an aqueous solution. A purpose-built processing plant needs to be designed and constructed on-site. Often a pilot plant is built first as a proof of concept and to identify and iron out the bugs before raising capital (issuing more shares) to build the final full production plant.

The process will typically create either lithium hydroxide or lithium carbonate, which is then sent to buyers who further process the compounds into their final form (hopefully, battery-grade Lithium).

Hard rock mining can take from 10 to 20 years from exploration through to the first production. And in the race to produce more lithium, speed to market is important.

Spodumene is the most commonly occurring lithium hard-rock mineral, which, once upon a time, made it the number one source of lithium metal in the world. It has since been surpassed by brines, which, for a number of reasons, have become the largest contributor to lithium production.

Lithium Brine

Lithium is concentrated in salt deposits already in the ground, and brine mining is a much simpler and faster technique than hard rock mining, Brine, typically carrying 200–1,400 milligrams per litre of lithium, is pumped to the surface and concentrated by evaporation in ponds.

Depending on pond depth, height above sea level and local weather, concentration by evaporation can take from 3 to 9 months. A concentrate of 1 to 2% lithium is further processed in a chemical plant to provide various end products, such as lithium carbonate and lithium hydroxide.

The Lithium chemistry can become complex particularly since the brine can also contain other troublesome elements such as magnesium.

However, lithium brine processing costs much less, is faster, and the best resources can deliver 99.9% purity, higher than possible from hard rock mining.

The Lithium Triangle

South America currently supplies 50% of the world’s lithium from a region known as the Lithium Triangle that spans the borders of Chile, Bolivia and Argentina. The region holds 54% of the world’s currently known lithium reserves.

Climatic conditions are perfect for evaporation and the briny waters underground have high concentrations of lithium salts.

While traditionally Chile has to lead the way for Lithium production, Argentina is emerging as the new Lithium Powerhouse.

A new government led by president Macri took over in December 2015 and has embarked on a major and much-needed shift in economic policies. Macri has declared 'Argentina open for business and new lithium mining ventures in Argentina's corner of Lithium triangle are finding a favorable government. Bolivia remains difficult.

Alternative sources of lithium

The conventional wisdom is Hard Rock Mining and Lithium Brine are the only two viable methods of unlocking lithium from its naturally occurring origins. But, that's based on current lithium prices and limited research into other methods.

The largest repository of lithium is the world's oceans, however at low concentrations. But research is underway to work out how to cost-effectively extract seawater lithium using dialysis, exploiting the tiny size of the lithium-ion.

With the price of lithium soaring to new heights and the huge levels of increasing market demand, the impetus to develop new extraction techniques and to refine existing techniques is compelling.

Increasing prices are shifting the return on investment equation.

Don't rule out the possibility that previously uneconomic sources of lithium will become viable and/or new sources will be discovered.

Lithium demand drivers

Well, that’s where Lithium comes from, the interesting point is where it's heading.

World Lithium demand is difficult to forecast now because demand keeps increasing and reliable data is hard to get. Lithium is not yet listed as a tradable commodity which makes investment confidence tricky. Debt finance can be difficult to find.

Around the globe, automakers and governments are betting big on electric cars. The numbers being projected are huge; by 2040, Bloomberg New Energy Finance estimates there will be 530 million electric vehicles in use. However, despite the hype, electric cars aren’t yet ‘popular’. In 2017, they made up about 1 per cent of global sales.

Electric vehicles are rapidly getting cheaper and range between charging is improving. And in some countries, government incentives are being used to encourage purchase.

Norway is by far the world leader in electric cars where zero-emission vehicles make up almost 30% of the total market.

Toyota launched the Prius, a petrol-electric hybrid, in 2000. Tesla helped revive interest by tarting up electric’s frumpy image-producing more elegant and higher performing vehicles.

Electric vehicles - The long tail pipe problem

Logical thinkers Initially deduced that electric cars were no better for the environment citing “the long tailpipe” concept; the idea that electric cars simply shifted the place where fossil fuels were burnt back to the power station supplying their charging electricity.

Electric car proponents argue that home solar will address this through solar panels. Cars will recharge overnight at home. Small problem, the sun doesn't shine at night. And charging a home solar battery during the day to charge an electric car battery at night is nuts.

Maybe the power generation industry will transform to renewables addressing this concern. A lot of expensive cogs have to fall into place.

The shortage of charging stations remains a significant hurdle (or a business opportunity). One wonders the effect this will have on already maxed out electricity grids.

Despite flaws in the logic, electric vehicles feature prominently in the climate change narrative. Buying an electric car signals virtue. No longer just for tree huggers; electric is going mainstream. And the business opportunities are huge.

For many, there is good reason not to question the fundamental assumptions; and most people seem to like the whole climate change zeitgeist; it's defining the current generation.

There's just too much emotion, reputation, and investment to contemplate the possibility that the assumptions are wrong. Belief defines its own logic.

With change comes opportunity.

Recently, major car manufacturers have started jumping on the electric wagon; even traditional European luxury brands are all well into development and are starting to release electric vehicles.

A production version of the 2015 Porsche Mission E electric concept is scheduled to go on sale at the end of 2019.

Mercedes’ new SLS AMG Coupé Electric Drive, the fastest electrically-powered series production car in the world caused a sensation at its premiere at the Paris Motor Show.

BMW has debuted its all-electric BMW i3 and BMW i8 hybrid.

Volkswagen, which has gone from being famous for that funny little car to being the worlds largest vehicle maker (having bought Lamborghini, Porsche, Bentley, Bugatti, Scania, Audi. Seat, Ducati, Skoda, and MAN) is planning a range of 23 VW-brand electric cars by 2025 and 50 EVs across its 12 brands. To be able to meet these targets, VW is building four battery gigafactories, in partnership with local and international partners.

Bosch, another German company and the world’s largest supply chain partner to the global automotive industry, could be one of these partners as the company is looking to invest in battery cell production.

Volvo plans to drop vehicles powered solely by internal combustion in 2019, moving to electric or hybrid only.

The Bloomberg New Energy Finance forecast says the take-up of emission-free vehicles will happen more rapidly than previously estimated because the affordability of buying electric cars is improving fast.

And with the imminent deployment of autonomous vehicles, the range between charging becomes less of an issue; a car that drives itself can also wander off and find someplace to juice up.

Lithium market dynamics

The first seismic shift in market dynamics will be the decline in global demand for oil. The global petroleum industry is already going through massive change with the OPEC cartel losing market share and attempting to hurt its rivals by dropping prices.

Oil prices went from over $110 per barrel in mid-2014 to now sitting well below $50.

Secondly, the traditional supply chain that manufacturers internal combustion engines will also need to retool for the future. The design of electric cars is significantly different to conventional cars affecting the entire automotive supply chain; underfloor batteries change seat designs, gearbox requirements require a total rethink (because there probably won't be one), braking systems, suspension – everything.

When (and if) electric vehicles take over from traditional internal combustion - the demand for oil will drop dramatically. Some think the sun is setting on Big Oil.

While traditional car suppliers may be disrupted by EV growth, some commodities will get a lift, according to BNEF:

- Graphite demand will soar to 852,000 tons a year in 2030 from just 13,000 tons in 2015

- Nickel and aluminium demand will both see demand from EVs rise to about 327,000 tons a year from just 5,000 tons in 2015

- Production of lithium, cobalt and manganese will each increase more than 100-fold

- And electric motors will need billions of miles of copper wire.

Currently, Lithium is still traded privately with battery manufacturers negotiating supply contracts direct with producers.

What is the price of Lithium?

Determining the price for Lithium is difficult.

Estimates vary widely, from USD$7,000 per tonne for Chinese imports of carbonate to USD$20,000 a tonne on the Chinese spot market for battery-grade material. However, there are also reports of the Chinese only paying USD$5,000 for US imports, according to analysts at Macquarie Bank.

Nobody knows for sure and, in any case, it changes with each new supply contract signed.

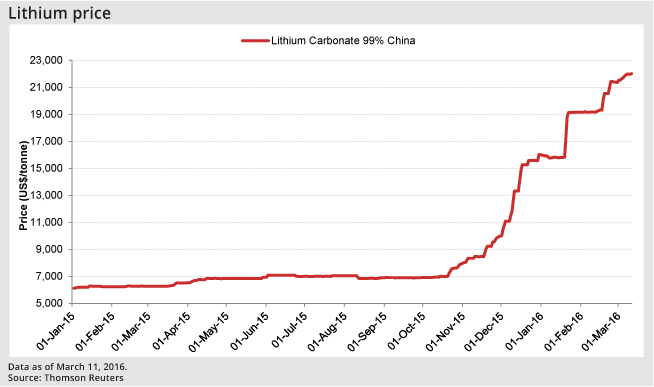

No matter which statistic you rely on, prices are increasing. CRU estimates that the Chinese spot price has almost tripled from USD$7,000 in the middle of 2016 to now being over USD$21,000. Chinese import prices for carbonate and export prices for hydroxide have hit record highs.

Price estimates rely on published trade volumes and trade values, a statistical sleuthing exercise made more difficult by the complexity of the lithium product chain. Lithium comes in many grades and in at least two compounds (carbonate and hydroxide).

However, at the time of writing this article, the generally discussed price of battery-grade lithium carbonate is around USD$25,000 per tonne. However, this could increase to well over USD$30,000 per tonne in the next 12 months.

Some commentators think it's possible the price on some transactions could even reach $100,000 per tonne*.

* Youtube video [Mike Beck presentation]

Lithium market size - volume and price

A credible attempt at estimating the global Lithium market is presented in this article [ Seeking Alpha: Tesla's Model 3 Launch: Where Will The Lithium Come From? ] it presents a comprehensive table listing current Lithium suppliers and volumes.

The total market size for lithium (2017) is estimated at 244,084 tons (221,429 metric tonnes) per annum.

The same article pegs the average price of lithium at USD$18,064 per tonne.

This suggests that the global value of the Lithium market is currently at USD$18 billion. However, the article also demonstrates that demand is already exceeding supply, so this market estimate is rapidly increasing.

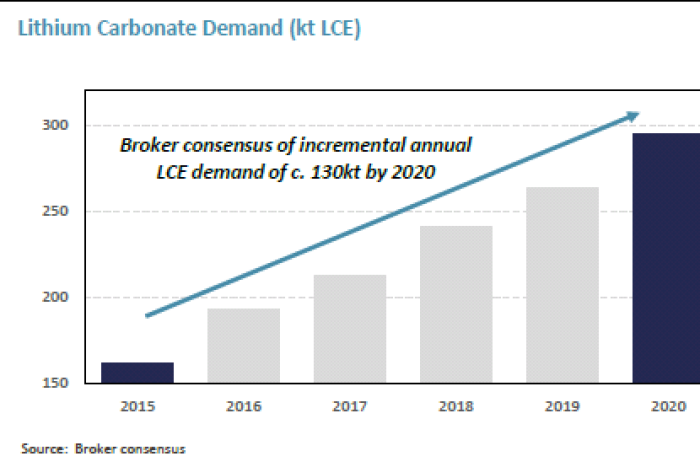

Lithium forecast market demand

The chart sourced from: ABC News Online: Why lithium is such a hot item right now. shows the dramatic forecast growth in Lithium demand that existing and new suppliers will be fighting to supply.

Little wonder prices will escalate dramatically.

Current lithium supply dominated by a few players.

Only four producers control about 85% of supply, Macquarie says.

Chile’s SQM, US companies FMC Corp and Albemarle Corp dominate the production landscape, extracting lithium from salt lakes in Chile and Argentina. Albemarle also operates a brine operation in Nevada.

The fourth producer is Australia’s Talison, which produces lithium at the Greenbushes mine in Western Australia.

For Tesla, the limited supply options is a problem. Tesla requires an estimated 27,000 tons of lithium carbonate a year to reach its sales target of 500,000 vehicles per annum by the end of 2018. That equates to 16% of global consumption last year.

The Lithium 'Gold Rush'

There is no shortage of other companies staking their claims to profit from the expected lithium gold rush.

A plethora of lithium explorers have listed all in various stages of resource development.

Noting, of course, that "various stages of development" means anything FROM "we're looking but haven't found anything yet" TO "we're setting up production, but haven't produced anything yet."

Fitting the above definition, the following Lithium plays are currently listed on the ASX; Argosy Minerals, Pilbara Minerals Ltd, Altura Mining Ltd. Tawana Resources, Avz Minerals Ltd, Birimian, Kidman Resources, Anson Resources, Greenpower Energy, Core Exploration, Lithium Power International, Sayona Mining, Estrella Resources, Lake Resources, Orocobre, European Metals Holdings, Global Geoscience, Prospect Resources, Carbine Tungsten, Reedy Lagoon Corporation, Caeneus Minerals. Pilbara Minerals, Pioneer Resources, Galaxy Resources, Neometals, and Mustang Resources.

That’s quite a list and that’s just the ASX.

The demand for Lithium is having a dramatic effect on share prices...

While in the short term, demand will certainly outstrip supply, this may change when all the new producers come online.

However, there is legitimate concern regarding the viability of many of these projects.

Some are attempting hard rock operations and are yet to prove up their resource and establish if viable extraction is possible. Others lack the expertise to efficiently extract Lithium from brines (it can be tricky), so there is much uncertainty that high volume supply will come online fast enough to service the growing demand. In the meantime share prices for the successful producers will rise rapidly.

Lithium off-take agreements

For a junior miner at pre-production, a significant price catalyst, sure to push the share price up, is the signing of an off-take agreement.

In the Lithium space, an off-take agreement is when a Tesla or other battery maker does a deal with the Lithium miner to buy an agreed tonnage of their first product.

Such off-take agreements are being signed 6 to 12 months before the mine is ready to produce its first batch.

This is seen by the market as clear evidence that the mine will be successful as securing a paying customer is what it's all about.

To secure Lithium supply, some battery makers are paying up-front for the first output

...providing funding for completing the mine development.

Again the share market likes this because it reduces or avoids the need for a capital raise which will dilute existing shareholdings.

However, in the current market, some of the more savvy miners are delaying signing off-take agreements as long as possible, for exactly the same reason the battery manufacturers want to lock them in now. The price is rising rapidly, by delaying signing any off-take agreements they can maximize the price.

Consequently, there is a widespread of share prices for emerging lithium stocks. Some of the lower-priced miners (down around the 20 cents to 30 cents range) who don't have off-take agreements - may be the highest-priced stocks in 12 months to 2 years.

But, here's the tricky bit. Do they not have an off-take agreement because buyers doubt project feasibility or are the resource playing hard-to-get?

It's complex, to say the least.

What about alternative battery technologies?

The question is, will somebody invent a new battery technology that renders lithium batteries obsolete?

A new battery technology would need some or all of the following advantages to knock lithium off its perch...

- Cheaper

- Lighter

- Higher energy density (cram more usable energy into a smaller package)

- Less prone to fire/explosion (remember the Samsung Galaxy 7 episode?)

- Longer life (Lithium batteries deteriorate over time & cycling)

- More tolerant to deep cycling (full charge / full discharge)

Lithium battery proponents (those betting their house on Lithium stocks) will tell you the battery industry is too deeply invested in lithium to want to re-gear for new technology, and/or a new battery breakthrough is years away. However, there are many researchers working on new technologies. And don't forget the story of Kodak that was too invested in film processing to seriously invest in the digital imaging system that it invented (filed for bankruptcy January 2012).

Labs all over the world are working on next-generation batteries.

Sodium Glass Battery

Recent developments include a [glass sodium battery] that uses commonly available sodium (easily separated from seawater) and a glass-based electrolyte. It provides another advantage of fast charging (the solid barrier between the anode and cathode prevents short circuits caused by the formation of dendrites).

Early results are very promising and commercial versions aren't far away with the research team currently working with battery makers.

Graphene supercapacitors

A capacitor is an extremely common device that stores electricity using an electrostatic charge; they've been around almost for as long as electricity has been identified.

Almost every electronic device includes many capacitors where they are commonly used to block, filter, or usefully change the characteristics of currents flowing through electrical circuits. Coupled with an inductor (coils of wire that store electricity using magnetic fields) they form electrical resonators and oscillators.

However, as energy storage devices they are commonly used in electronic flashguns, cardiac defibrillators, electronic ignitions etc. where their stored energy can be released suddenly to generate very high voltages.

A supercapacitor is basically a very big capacitor. Researchers are attempting to build supercapacitors using graphene; a remarkable super material promising strength and lightweight. A working version is a way off yet, but watch the supercapacitor space.

Redox Flow Batteries

Basically, a more complicated version of standard battery technology (using an electrolyte between two dissimilar metals to create chemical energy storage) the Redox battery enhances this effect by using two electrolytes instead of one. They promise lightweight and offer up to four times the lifespan and much greater storage.

The prototypes are still in the lab, for a more complete list of the latest battery research [read more here]. In summary, yes plenty of research is being thrown into alternatives to Lithium so it's not so much a matter of IF only WHEN.

With the price of Lithium skyrocketing and its lack of availability hampering the electric vehicle and renewable energy revolution, the impetus to find alternatives is becoming more compelling.

However, right now, Lithium-based battery technology is the market leader, facilitating the renewable energy revolution.

While the future is uncertain, several facts can be banked on…

- Global demand for lithium is rapidly increasing and is outstripping the current supply.

- As would be expected, prices for lithium are being pushed up rapidly.

- Development of new lithium resources is progressing at a fever pitch pace.

- 5 Year Window. Taking into account growth in demand and growth in supply, and the high likelihood that new battery technology will emerge, there is probably a 5-year window before alternative technologies reach the market.

- Huge risk. Right now there appears to be ample justification for forecasting huge increases in the price of lithium. The current supply is low and demand is already huge and growing and lithium is a small fraction of the price of an electric vehicle. But, necessity is the mother of invention.

The whole "we'll all be rich!" pitch, rests on no new technologies and supply not catching up with demand. Feeling lucky?

It will be interesting to see where the market for Lithium ends up. But tread carefully, with every boom comes the bust.

Read more about the global demand for Lithium...

- Mike Beck: Lithium - The Perfect Storm with an Unprecedented Demand Profile

- What Price Lithium, the Metal of the Future?

- visualcapitalist.com/a-cost-comparison-lithium-brine-vs-hard-rock-exploration

- energyandcapital.com/report/making-money-from-the-true-future-of-lithium-brine-vs-hard-rock/2157

- mining.com/web/lithium-supply-demand-story

- bloomberg.com/quicktake/electric-vehicles

- bloomberg.com/news/articles/2017-07-06/the-electric-car-revolution-is-accelerating

- economist.com/news/americas/21723451-three-south-american-countries-have-much-worlds-lithium-they-take-very-different

- Stanford News: Battery based on sodium may offer more cost-effective storage than lithium

- Glass sodium battery - 3 times the energy density of Lithium

- Ten alternatives to Lithium batteries

- A credible estimate of demand, current volume, and pricing of Lithium

- Must view: Mike Beck: Nickel, Cobalt, and Lithium to Benefit From Generational Demand Shift in Commodities [Youtube] - "Lithium to reach $100k per ton"

- Extracting lithium from the sea